401k and pensions

-

Questions about this, and I apologize for asking before research. Call it being a conversationalist or being lazy or bringing those playing at home along for the mental process (yeah, thats it!)

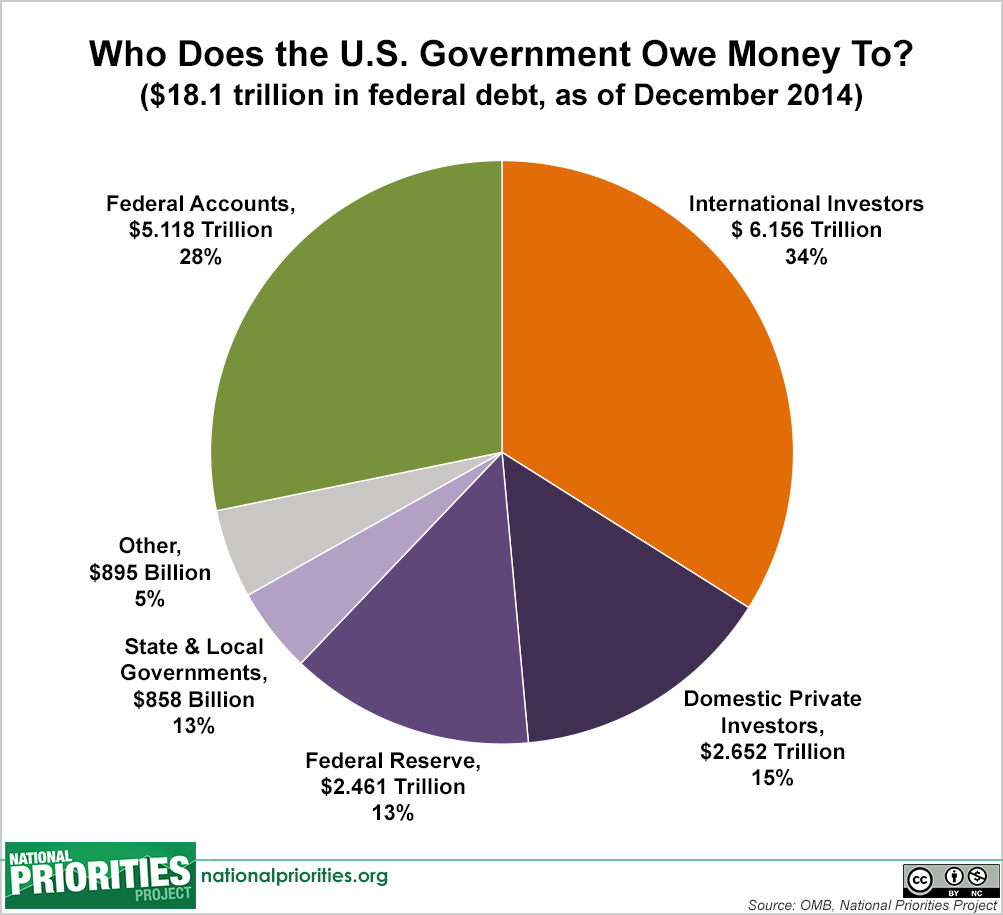

So if we increase interest rates can we increase the debt in certain sectors of this graph? For instance, can we only sell bonds to domestic entities?

And more broadly, is there a creative way to increase interest rates that hasnt been explored?

@approxinfinity said in 401k and pensions:

Questions about this, and I apologize for asking before research. Call it being a conversationalist or being lazy or bringing those playing at home along for the mental process (yeah, thats it!)

So if we increase interest rates can we increase the debt in certain sectors of this graph? For instance, can we only sell bonds to domestic entities?

And more broadly, is there a creative way to increase interest rates that hasnt been explored?

I love this stuff so it’s good! The issues are 1) debt is postponing future taxes; 2) sovereign debt crowds out private investment and slows growth. A good example of this is Japan. Their debt burden is extremely high and they haven’t grown much for decades. Increasing debt service payments also has the effect of increasing taxes on us all or replacing other programs that could be useful. Our tax money is increasingly just paying bondholders instead of other uses like paying down debt, bolstering defense, or whichever programs we could prioritize. The crowding out effect is where private money goes to Treasuries instead of venture capital, stocks, or other investments that could actually grow the economy. It’s ok in an emergency but, kind of like your household, you don’t want to rack up high interest credit card debt in your everyday life.

-

@approxinfinity said in 401k and pensions:

Questions about this, and I apologize for asking before research. Call it being a conversationalist or being lazy or bringing those playing at home along for the mental process (yeah, thats it!)

So if we increase interest rates can we increase the debt in certain sectors of this graph? For instance, can we only sell bonds to domestic entities?

And more broadly, is there a creative way to increase interest rates that hasnt been explored?

I love this stuff so it’s good! The issues are 1) debt is postponing future taxes; 2) sovereign debt crowds out private investment and slows growth. A good example of this is Japan. Their debt burden is extremely high and they haven’t grown much for decades. Increasing debt service payments also has the effect of increasing taxes on us all or replacing other programs that could be useful. Our tax money is increasingly just paying bondholders instead of other uses like paying down debt, bolstering defense, or whichever programs we could prioritize. The crowding out effect is where private money goes to Treasuries instead of venture capital, stocks, or other investments that could actually grow the economy. It’s ok in an emergency but, kind of like your household, you don’t want to rack up high interest credit card debt in your everyday life.

@RedLyonRegular alright, so it seems like what i want is for the fed rate to be 6% instead of the 3.88% it is at now.

This makes savings interest rates of 5% feasible.

It slows the tech and growth stocks. I want this, this kneecaps the tech sector and loosens Wall Streets chokehold on our economy.

It raises interest rates on loans and slows the economy. I want this, it forces the houses and automarkets to stop inflating the cost of houses and cars. It stops people from taking on debt they cant repay.

It slows inflation. We want this. We want interest rates to outpace inflation.

In addition to keeping inflation low if we can break up monopolies, we keep companies from arbitrarily jacking prices.

… why arent we doing this @RedLyonRegular ?

")

-

I'm not an economist, but I enjoy reading about aspects of it and I've thought briefly about societal benefits to different types of retirements. So, my quick take on that is that you have issues of trust on both sides. If you have a defined-contribution retirement account (like a 401K; a less US-centric term), then you put trust in the individual and avoid the issue of trusting the entity that would be doling out pensions (whether company or government). This means you take on the risk of some people saving too little, or living much longer than they expect. If this happens, what do you do with elderly folks that don't have a source of income or family to take care of them? It's inhumane to let them die on the street, so you want some kind of safety net. In a place with robust safety nets, maybe those apply well enough to old people that you don't need something special. If you have a defined-benefit plan (pension), then you trust the entity administering it rather than the person. If it's a company, you trust them not to go out of business or shadily change the terms of the pension. If it's a government, you trust them to model demographics and fund appropriately so that the system remains solvent. There are issues of tying up that capital where young workers can't use it for things like housing, which can harm the economy in certain circumstances. So, personally I am a fan of defined-contribution plans as the primary retirement income--what people rely on for living a good, comfortable life. But, you have a government safety net that gives basic quality of life to those who don't have enough retirement. Of course, there are plenty more questions on the size of contributions, etc that can have major effects.

In terms of interest rates (and many things), I like the golden mean approach. Having rates too close to 0 causes problems but so does having high rates. @approxinfinity while low interest rates can help the tech sector, I don't think that high rates do much to cripple it--other sectors would likely be hit first. In terms of collective action, I think having better regulations on interest rate disclosures and speed of changing would be most impactful. For the US, re-teeth the CFPB and institute some laws about how much rates can be changed within a year (maybe with exceptions when the Fed changes by more than that amount). This could help avoid predatory lending and banks giving a high interest rate for a short period to get people to start accounts, then lowering it (causing the switching cost dilemma for people).

-

@pastvulcan gotcha. While defined-contribution retirement over defined-benefit retirement does seem to be the consensus, i think the question i have is whether we can move it away from stocks. I had been kind of throwing “401k” around meaning “managed fund”, which typically is in large part stocks. As @RedLyonRegular pointed out, we can elect to put 401ks into bonds but that definitely isnt the norm.

So my question i think with a little more precision is “can we make the interest rates on other managed fund options besides stocks competitive? And can we force a mix that is less stock heavy?” theres plenty of runway i think still to discuss what the effect of that may be on companies and on the economy.

I will have to read up more on what the recent dismantling of the CFPB means for consumers, it sounds like there are still laws like the Truth In Lending Act but the CFPB was the main agency to enforce that. Thanks for bringing this up.

-

@RedLyonRegular alright, so it seems like what i want is for the fed rate to be 6% instead of the 3.88% it is at now.

This makes savings interest rates of 5% feasible.

It slows the tech and growth stocks. I want this, this kneecaps the tech sector and loosens Wall Streets chokehold on our economy.

It raises interest rates on loans and slows the economy. I want this, it forces the houses and automarkets to stop inflating the cost of houses and cars. It stops people from taking on debt they cant repay.

It slows inflation. We want this. We want interest rates to outpace inflation.

In addition to keeping inflation low if we can break up monopolies, we keep companies from arbitrarily jacking prices.

… why arent we doing this @RedLyonRegular ?

@approxinfinity it does a lot of the opposite. Small businesses rely on lines of credit throughout the year to smooth over seasonal fluctuations. Raising rates on those when margins are already small would make it even harder to stay afloat. It also slows consumer spending, as anyone with debt sees a bigger piece of their budget go to interest payments instead of buying stuff from Mom and Pop, Inc., and that’s not even considering the brutal effect on the country’s fiscal situation. Amazon will be fine, it’s the businesses on the edge of making it that will go under. Which destroys a lot of jobs and livelihoods. When Volcker cranked up rates north of 20%, unemployment rose to almost 11%.

That’s not to say low rates fix everything, too low rates can cause bubbles in some sectors (e.g. housing, dot com) which is really not good. So it’s up to the Fed to weigh all these factors and set their target. Overall I think we’re in a good spot in that regard. Are prices too high? In some places yes. Cutting tariffs would be a good place to start.

-

@approxinfinity it does a lot of the opposite. Small businesses rely on lines of credit throughout the year to smooth over seasonal fluctuations. Raising rates on those when margins are already small would make it even harder to stay afloat. It also slows consumer spending, as anyone with debt sees a bigger piece of their budget go to interest payments instead of buying stuff from Mom and Pop, Inc., and that’s not even considering the brutal effect on the country’s fiscal situation. Amazon will be fine, it’s the businesses on the edge of making it that will go under. Which destroys a lot of jobs and livelihoods. When Volcker cranked up rates north of 20%, unemployment rose to almost 11%.

That’s not to say low rates fix everything, too low rates can cause bubbles in some sectors (e.g. housing, dot com) which is really not good. So it’s up to the Fed to weigh all these factors and set their target. Overall I think we’re in a good spot in that regard. Are prices too high? In some places yes. Cutting tariffs would be a good place to start.

@RedLyonRegular couldnt we have legislation that offers better rates to small businesses than to large corporations? We have the opposite going on with advantages being given to big business like local tax write offs for amazon to move to an area. Shouldnt we do the opposite and incentivize small business? It seems like instead of writing off increased interest rates because they havent worked, we could nuance the laws around them so they could work while getting the desired benefits?

-

@unshittified it sounds like you're proposing forcing banks to offer differential loan rates, which definitely seems like dangerous territory. The Small Business Administration already helps small businesses get loans, though I think it's more guaranteeing the loans to get competitive rates and matching with lenders, not subsidizing the rates. The federal competitive advantage to small, minority-owned businesses provide a cautionary tale. Sometimes, a contract will go to a small business that immediately subcontracts to a large defense contractors, with the main effect of raising costs.

While I don't think there are easy solutions, my thought in both cases is to help even the playing field before selection, rather than putting a thumb on the scales. In the case of small and minority-owned businesses, providing free mentoring and training (on the federal bids process, among other things) to everyone would help them know how to compete with larger firms that already know the process. You can get around affirmative action pushback by offering to everyone, but expecting that the bigger beneficiaries are folks that started with a disadvantage. For interest rates, I think the existing SBA items (properly funded) and restricting huge corporations in other ways that limit their power would be more effective than trying to fix the rates beyond what the Fed already does. As Doctorow discusses, there are relatively administrable remedies such as requiring companies to not compete with their customers (like Google/Apple app copies in their appstores, or Amazon looking at top selling products and offering their own). Making Amazon pay full corporate tax would help more than raising their interest rates. On the tax writeoffs, I actually think that's a case where paternalism is reasonable: the federal government should preempt tax writeoffs by states and localities beyond a certain amount (say, the actual amount taxes are lowered should be less than 5% of the total taxable income of all employees living in that locality). There are other harmful ways local officials can tempt companies, so this would just be a first salvo.

-

Thanks @pastvulcan.

I like the idea of tying the business write off to the employee income. Has that ever been considered i wonder?

Regarding google apple and amazon not competing (also, in store brand in all the grocery stores) with their business customers, i guess they could be forced to sell off those arms of their company that produce those things.

-

Thanks @pastvulcan.

I like the idea of tying the business write off to the employee income. Has that ever been considered i wonder?

Regarding google apple and amazon not competing (also, in store brand in all the grocery stores) with their business customers, i guess they could be forced to sell off those arms of their company that produce those things.

@unshittified said in 401k and pensions:

Regarding google apple and amazon not competing (also, in store brand in all the grocery stores) with their business customers, i guess they could be forced to sell off those arms of their company that produce those things.

Easier said that done. What part of Amazon is the business customer and what part is the platform? A lot of people have proposed the kind of split you propose and, AFAIK, the companies hide behind the difficulty in drawing the line. Just for example, I work in Replenishment. And that's both for Walmart and for 3rd Party sellers. Ha! Apple might be the easiest case, since it's not competing but rather stealing from its "business customers". I think Epic Games vs. Apple would seem to be the best development in years on that front. But let's see how much things really change. FWIW I'm with you. But the details are so tricky and the companies so lawyered up, etc.

-

@ilam.fields you bring up some great points.

I have a sneaking suspicion as I get farther reading Unshittification and we explore how best to educate the people on the woes of enshittification, that Cory has already turned over these rocks, and the immediate solutions, at least in the short term, will not be litigation, but rather collective action.